Microsoft’s latest market bump isn’t trivia — it’s a narrative built on a Morgan Stanley CIO survey that places the company as the primary beneficiary of a modest but consequential rise in corporate software budgets, and that market narrative is already shaping investor expectations, product road maps and CIO procurement plans.

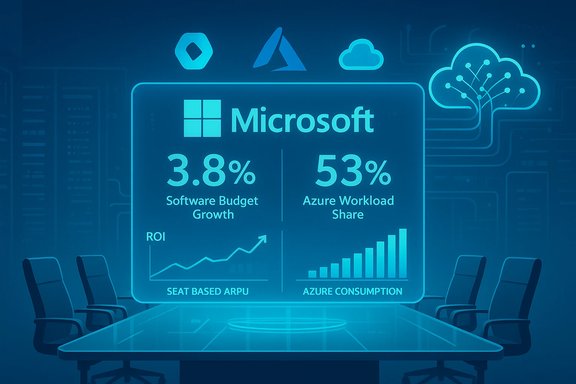

The Morgan Stanley CIO survey at the center of recent coverage signals a modest acceleration in corporate software budgets — roughly 3.8% year-over-year growth projected for 2026 — and identifies Microsoft as the top expected beneficiary of that incremental spending. That single datapoint has been repeated across market write-ups and analyst notes, and it underpins a widely circulated thesis: seat-based software upgrades (Microsoft 365 and Dynamics), coupled with Azure consumption for AI inference and hosting, create a compound monetization path for Microsoft.

Why the survey matters is straightforward: when CIOs intend to prioritize one vendor for new projects, procurement creates a vector that can convert into both recurring subscription revenue (seats) and incremental cloud consumption (compute, storage, inference). The survey reports that approximately 53% of surveyed application workloads already run on Azure, and it shows substantial intent to adopt Microsoft’s Copilot family, GitHub Copilot, and Azure OpenAI services — signals that collectively explain why some analysts re-rated Microsoft’s near-term opportunity set.

That said, the headline optimism should be calibrated with sober execution checks. Investors need to weigh the probability of a smooth seat-to-cloud conversion and efficient infrastructure scaling against the present premium valuation. CIOs and IT leaders should treat the findings as a practical prompt to test Microsoft products under strict FinOps and governance regimes rather than as an unconditional green light to accelerate enterprise-wide rollouts.

However, intent alone is not destiny. Converting CIO preference into durable, margin-expanding revenue requires Microsoft to execute on datacenter capacity, manage infrastructure economics, and keep competitive and partner dynamics favorable. CIOs and investors should treat the Morgan Stanley signals as an actionable lead: plan pilots, enforce FinOps and governance, and measure conversion rates from intent to booked revenue — because those metrics, not headlines, will determine whether the market’s optimism is ultimately justified.

Source: Finviz https://finviz.com/news/279283/micr...rising-software-spending-morgan-stanley-says]

Background

Background

The Morgan Stanley CIO survey at the center of recent coverage signals a modest acceleration in corporate software budgets — roughly 3.8% year-over-year growth projected for 2026 — and identifies Microsoft as the top expected beneficiary of that incremental spending. That single datapoint has been repeated across market write-ups and analyst notes, and it underpins a widely circulated thesis: seat-based software upgrades (Microsoft 365 and Dynamics), coupled with Azure consumption for AI inference and hosting, create a compound monetization path for Microsoft.Why the survey matters is straightforward: when CIOs intend to prioritize one vendor for new projects, procurement creates a vector that can convert into both recurring subscription revenue (seats) and incremental cloud consumption (compute, storage, inference). The survey reports that approximately 53% of surveyed application workloads already run on Azure, and it shows substantial intent to adopt Microsoft’s Copilot family, GitHub Copilot, and Azure OpenAI services — signals that collectively explain why some analysts re-rated Microsoft’s near-term opportunity set.

What the Morgan Stanley Survey Actually Reports

Headline numbers

- Software budget growth expectation: ~3.8% for 2026 (a modest acceleration versus prior year expectations).

- Azure workload presence in the surveyed cohort: ~53% of application workloads reported on Azure.

- Adoption intentions (sample highlights): ~37% planning to use Azure OpenAI Services within 12 months; ~42% planning to use GitHub Copilot; Microsoft 365 Copilot intent reported substantially higher in the same sample.

What “#1 share gainer” means in practice

Morgan Stanley frames Microsoft as the likely “share gainer” from the incremental IT wallet driven by cloud migration and AI initiatives. The reasoning is pragmatic: Microsoft controls high‑share productivity suites (Microsoft 365), enterprise identity and governance (Azure AD, Purview), and an expanding set of AI capabilities that are easiest to deploy when the organization is already running its application workloads and identities on Azure. That combination increases switching costs and creates natural consumption anchors for Azure inference and storage.Why the Market Reacted: The Seat + Consumption Compound

Microsoft’s monetization architecture is unusually well-aligned with the survey’s signals. The company captures value in two linked ways:- Seat monetization: upgrading Microsoft 365 seats to Copilot-enabled SKUs or higher-tier licenses increases average revenue per user (ARPU).

- Consumption monetization: Copilot and other AI features use inference and storage that run on Azure, generating metered cloud revenue.

Verifying the Claims and Their Limits

Triangulation and independent confirmation

The most load-bearing numeric claims from the Morgan Stanley survey — the 3.8% software budget growth and the ~53% Azure workload share — have been reported across multiple outlets covering the same research note. That triangulation increases confidence that the figures are accurately summarized from Morgan Stanley’s work rather than misreported by a single outlet. However, these are survey results, not audited market-share measurements, and they reflect the distribution and composition of the survey’s respondents rather than a census of global enterprise workloads.Survey limitations (why intent is not revenue)

- Surveys measure intent, not binding contracts. Procurement cycles, compliance reviews, and pilot-to-production conversion rates materially affect revenue realization.

- Sample composition matters: industry mix, company size and regional distribution can skew workload statistics — a vertical-heavy or cloud-early sample will show higher Azure penetration than a random global sample.

- Short-term execution constraints — capacity, tooling and governance — can delay recognition of spend even where CIO intent is strong.

Product-Level Implications for Microsoft

Azure: from hosting to margin driver

If enterprises run the majority of their application workloads on Azure within the surveyed cohort, Microsoft gains the first call on AI-related compute and storage when organizations scale Copilot or other generative AI features. That’s meaningful because AI inference is metered and typically has a higher direct cost-per-workload profile than traditional cloud compute. For Microsoft, higher Azure utilization tied directly to seat monetization can create a durable cloud revenue stream, but only if Microsoft manages infrastructure economics (datacenter capacity, GPU availability, power and cooling, and procurement) efficiently.Microsoft 365 Copilot and seat uplift

Copilot represents a specific and visible path to raise ARPU across Microsoft 365, converting long-standing seat economics into higher-value subscriptions. The combination of increased list prices on certain SKUs and the attach rates for AI features accelerates the potential for revenue per user to climb — but the attach rate and actual deployment speed are the critical conversion metrics. Analysts referencing the survey see Copilot attach as the leading top-line catalyst; actual financial uplift will depend on conversion and up-sell timing.GitHub Copilot and developer productivity

Developer tools like GitHub Copilot offer a different monetization cadence: smaller per-seat price tags but broad addressability and potential to accelerate development velocity (which many customers view as a cost-savings proxy). Corporate adoption here can also steer cloud workloads toward Azure if models and deployment tooling are tied to Microsoft’s ecosystem.Financial and Valuation Considerations

The upside case

Analysts bullish on Microsoft point to a few concrete near-term drivers:- Microsoft’s recurring revenue base and subscription anchors make additional ARPU easier to monetize than for more transactional vendors.

- Copilot adoption could lift average selling prices across installed seats, making the revenue base stickier.

- Azure’s potential to convert added seat features into metered consumption supports margin expansion over time if infrastructure scaling is managed efficiently.

The sensitivity to execution

Microsoft’s premium valuation makes the upside highly contingent on execution. Several risk factors can reduce upside or extend the timeline for impact:- Capital intensity: Scaling GPU-heavy infrastructure requires heavy capex that can weigh on margins in the short term.

- Procurement frictions: governance, privacy, and FinOps objections can delay or reduce adoption of inference-driven services.

- Competitive pressure and partner moves: OpenAI and other model providers are diversifying infrastructure partnerships, which can weaken exclusive assumptions about Azure being the sole inference home.

Operational Risks: Capacity, Cost and Governance

Datacenter capacity and GPU supply

AI workloads are both compute- and energy-intensive. If Microsoft cannot secure a cost-effective, scalable supply of accelerators (GPUs/TPUs) and balance that with energy and cooling requirements, Azure’s gross margins could be pressured even as revenue grows. Several analyst notes have highlighted the capital intensity of this infrastructure race as a central risk to near-term margin expansion.FinOps and visibility into inference cost

Organizations piloting Copilot-like experiences quickly learn that inference costs can scale nonlinearly as users shift from exploratory usage to production. Effective FinOps practices — metering per tenant, limiting model size or context windows, and setting guardrails on inference frequency — are required to keep consumption spend predictable. Survey intent to deploy is meaningful only if procurement teams can model and budget for that consumption.Data governance and compliance

Highly regulated sectors (healthcare, finance, government) demand auditable pipelines, data residency guarantees and provenance controls before they will trust generative models with production workloads. Microsoft has product pathways (Azure Government, Azure Arc, Purview) aimed at these needs, but enterprise adoption requires verified security and controls at scale — another conversion friction point.Competitive and Partnership Dynamics

OpenAI and the multi-partner reality

Microsoft’s early commercial relationship with OpenAI gave it a distinct advantage in AI productization. But the vendor landscape is evolving: model providers are seeking multi-cloud/partner strategies and enterprises are demanding supplier flexibility. If model providers or major customers opt for multi-cloud inference strategies, Microsoft’s exclusive leverage could weaken over time. Analysts note that OpenAI and others are expanding infrastructure partnerships, which changes assumptions about Azure being the automatic inference destination.Rival clouds: AWS and Google Cloud

Both AWS and Google Cloud are intensifying their AI offerings, with differentiated go-to-market approaches and deep integration into other parts of enterprise stacks. Microsoft’s hybrid strength (Windows Server, Azure Arc) and seat-based advantages remain differentiators, but competitors will fight aggressively on pricing, partner ecosystems and specialized AI tooling. The presence of strong competitors increases the bar for Microsoft to deliver both differentiated value and attractive economics for enterprise customers.Practical Recommendations for CIOs and IT Leaders

How to treat the Morgan Stanley signals in planning

- Use the survey as a directional indicator, not a procurement mandate. Treat reported intent as a prompt to evaluate vendors and re-run internal total-cost-of-ownership and FinOps forecasts.

- Pilot conservatively: run Copilot and Azure OpenAI projects in controlled environments with metering, budget alerts and rollback plans.

- Insist on governance: require traceability, data provenance and privacy-preserving training workflows before scaling generative AI into regulated workloads.

Tactical steps (numbered)

- Inventory existing seat spend and identify high-priority workloads for AI augmentation.

- Run a controlled pilot with clear KPIs tied to productivity, error reduction and cost impact.

- Implement tenant-level metering and FinOps rules to cap inference spend during pilots.

- Build an audit trail and compliance checks into model training and inference pipelines.

- Reassess vendor lock-in risk and evaluate multi-cloud or hybrid strategies where needed.

Strengths of the Morgan Stanley Case — and Where It Overstates

Notable strengths

- The survey captures CIO sentiment at a pivotal time when generative AI is moving from experiments to early production, making it a valuable leading indicator for procurement trends.

- Microsoft’s product breadth (Windows, Microsoft 365, Dynamics, Azure) and identity/management stack (Azure AD, Purview) create real, measurable switching costs that favor seat-to-cloud monetization.

- Early partner wins and documented deployments in regulated sectors (e.g., tax automation, government workloads) validate that real-world projects are progressing beyond proof-of-concept.

Where the thesis overstates the case

- Survey intent is not equivalent to booked revenue; the path from pilot to enterprise rollouts often spans multiple quarters or years, especially where governance and cost predictability are concerns.

- Infrastructure economics are nontrivial: higher Azure volumes can still produce margin pressure unless Microsoft scales GPU supply and energy efficiently. The capital intensity of this race is underemphasized in optimistic summaries.

- Competitive moves and multi-partner strategies among model providers could blunt Microsoft’s exclusive advantage if customers insist on multi-cloud portability for strategic resilience.

Editorial Judgment: How Investors and Practitioners Should Read This Moment

The Morgan Stanley survey is a meaningful and well‑timed datapoint that justifiably shifts attention toward Microsoft as a leading beneficiary of rising enterprise software spending and AI adoption. The combination of seat-based ARPU uplift and Azure consumption as complementary monetization levers is a plausible and attractive model.That said, the headline optimism should be calibrated with sober execution checks. Investors need to weigh the probability of a smooth seat-to-cloud conversion and efficient infrastructure scaling against the present premium valuation. CIOs and IT leaders should treat the findings as a practical prompt to test Microsoft products under strict FinOps and governance regimes rather than as an unconditional green light to accelerate enterprise-wide rollouts.

Conclusion

Morgan Stanley’s CIO survey has crystallized a compelling market narrative: rising software budgets plus AI interest are creating a platform advantage for Microsoft, with Copilot and Azure as the principal monetization engines. The numbers in the note — software budget growth of around 3.8% and a reported ~53% Azure workload share within the survey cohort — are powerful directional indicators that explain recent market reactions.However, intent alone is not destiny. Converting CIO preference into durable, margin-expanding revenue requires Microsoft to execute on datacenter capacity, manage infrastructure economics, and keep competitive and partner dynamics favorable. CIOs and investors should treat the Morgan Stanley signals as an actionable lead: plan pilots, enforce FinOps and governance, and measure conversion rates from intent to booked revenue — because those metrics, not headlines, will determine whether the market’s optimism is ultimately justified.

Source: Finviz https://finviz.com/news/279283/micr...rising-software-spending-morgan-stanley-says]